Finance & the Economy (2011-12)

Newer 'Finance & The Economy' posts can be found here.

Blame Game: The median net worth of American households has dropped to a 43-year low as the lower and middle classes appear poorer and less stable than they have been since 1969.

According to a recent study by New York University economics professor Edward N. Wolff, median net worth is at the decades-low figure of $57,000 (in 2010 dollars). And, as the numbers in his study reflect, the situation only appears worse when all the statistics are taken as a whole. The Average Joe is falling behind. According to a recent study by New York University economics professor Edward N. Wolff, median net worth is at the decades-low figure of $57,000 (in 2010 dollars). And, as the numbers in his study reflect, the situation only appears worse when all the statistics are taken as a whole. The Average Joe is falling behind.

According to Wolff, between 1983 and 2010, the percentage of households with less than $10,000 in assets (using constant 1995 dollars) rose from 30% to 37%. The "less than $10,000" figure includes the numerous households that have no assets at all, or a negative net worth.

The poor are getting poorer. Much of that poverty increase can be traced to bad habits/decisions: not finishing school/poor education, single parenting, welfare mentality. Consider this recent headline: 'Only 7% of Detroit Public-School 8th Graders Proficient in Reading'. Does anyone think that this kind of "education" is going produce a crop of career-flexible, productive adults? Or entrepreneurs? (I've written about the deficiencies of American schools on several occasions.)

Over that same period of time, the wealthiest 1% of American households increased their average net worth by 71%. The very rich are getting richer. From 1983 to 2010 the share of total wealth held by the richest 10% of American households increased from 68% to 77%. These are people who make wise choices, keep their eyes open for new career opportunities and pay attention to their spending and investments. They plan for the future and live within their means.

A Pew Research Center study found that many in the middle-class are divided on how they believe this gap widened.

85% of self-described middle-class adults say it is more difficult now than it was a decade ago to maintain their standard of living. Asked to point out the various culprits, 62% blamed Congress, 54% blamed banks and financial institutions, 47% faulted large corporations, 44% blamed the Bush administration, 39% pointed to foreign competition and 34% blamed the Obama administration. A mere 8% blamed themselves.

Here are the cold, hard facts: America has been undergoing a revolution. The corporate womb-to-tomb culture is dead. Job skills no longer last a lifetime because new technology makes old skills obsolete - quickly. In order to move up the ladder, one must constantly be on the lookout for new opportunities created by change.

The path to success now requires constant learning and skill upgrades. That's the new reality. Those who won't adapt - wishing for a return of The Good Old Days - will be the ones who will watch their standard of living continue to decline. And sadly, they'll have no one to blame but themselves. (posted 12-14-12, permalink)

Look Out Below! Headlines everywhere are screaming about driving off the fiscal cliff if there's no budget/debt deal in Washington, DC and sequestration kicks in.

Sequestration means that an amount of money equal to the difference between the cap set in the Congressional Budget Resolution and the amount actually appropriated is "sequestered" by the Treasury and not handed over to the agencies to which it was originally appropriated by Congress.

This is a forced balancing of the federal budget and supposed to inspire Congress and the President to come up with a more-palatable budget and a "solution" to our ever increasing debt.

I call bullshit on it. The Democratic-controlled Senate has not passed any budget in almost four years. How will this inspire them? Sequestration will not reduce our national debt, it will simply prevent it from increasing further. But hey, it's a beginning.

If these bozos fail to agree, we citizens get punished. If they were serious, they should be punishing themselves: fail to agree by the deadline and they get their own "fiscal cliff": no salary, no expense reimbursements and turn down the heat at the Capital and the White House to 45 degrees - just enough to protect the buildings. Not the occupants.

My sequestration plan would have all Congressional offices padlocked; temporary 'offices' will be in the hallways using card tables and folding chairs. All restrooms will be locked; senators and representatives will have to hike down to the Capitol Hill Exxon on Pennsylvania Avenue and beg for the bathroom key. Or, if it's already in use, trot over to the Sunoco station on aptly-named P Street. President Obama and his family must move out of the White House; he'll need to pay for his family's own food and lodging until an agreement is signed. Since the Sherlock Sequestration will also call for padlocking the United States Naval Observatory, expect to see Joe Biden and his family bunking at the Motel 6 on Georgia Avenue. My sequestration plan would have all Congressional offices padlocked; temporary 'offices' will be in the hallways using card tables and folding chairs. All restrooms will be locked; senators and representatives will have to hike down to the Capitol Hill Exxon on Pennsylvania Avenue and beg for the bathroom key. Or, if it's already in use, trot over to the Sunoco station on aptly-named P Street. President Obama and his family must move out of the White House; he'll need to pay for his family's own food and lodging until an agreement is signed. Since the Sherlock Sequestration will also call for padlocking the United States Naval Observatory, expect to see Joe Biden and his family bunking at the Motel 6 on Georgia Avenue.

My guess is that such an idea would bring about a quick solution. I bet Harry Reid, Mitch McConnell and Nancy Pelosi haven't experienced the joys of service station toilets in many years. And, when do you think was the last time that Obama had to pay a own hotel bill out of his own pocket?

Unfortunately, my idea will be ignored.

In theory, every federal agency will get a haircut under the sequestration proposed by legislators. However, Congress exempted certain very large programs from the sequestration process (Social Security and certain parts of the Defense budget). This would virtually cripple the activities of the unexempted programs. Maybe that's not such a bad thing.

Yes, it will suck if you're a defense contractor employee. On the other hand, PBS may go dark and they'll be no more government-subsidized Big Bird. Or preachy Bill Moyers. Heh. Hey, we're pulling out of Afghanistan in 2014 come Hell or high water and our enemies already know it. Sequestration will let us leave early and save American lives.

Social Security payroll deductions will markedly increase; that may help the solvency of this financially-troubled program. Federal tax withholdings will rise as tax rates rise. These two things will certainly wake up wage earners, when they suddenly experience reduced take-home pay.

Goodbye Federal Matching Programs. Farewell Pell Grants - wanna go to college? Get a part-time job like people used to. 'See ya' to all the mediocre sculptors underwritten by the National Endowment of the Arts. No more funding studies about the sex life of clams. Other cuts would include $150 million for healthy marriage promotion, $124 million for seat belt safety, $21 million for prisoner re-entry job searches and $7 million for motorcycle safety. There would be no more money for more government-backed solar panel or electric car start-ups.

Hey, I'm startin' to like this sequestration thing.

Here's a little joke for ya: "What do you call $1.2 trillion in automatic budget cuts?" A: "A good start."

Moody's is threatening to downgrade our financial rating ... again. (Meh. Those guys downgrade everything. Because they feel so depressed. Wouldn't you be semi-suicidal if your name was 'Moody'?) Mr. Moody doesn't like sequestration. So what? When the U.S. was downgraded earlier, it made big headlines. But did it make any difference in your life? Is your bank paying higher rates on CDs? I didn't think so. But ... but ... but ... the stock market's gonna tank. Haven't you noticed? It started doing so the day Obama got reelected.

Sequestration means everybody gets to share the pain ... including the poor who will see a tax increase. Many of those who haven't paid taxes in years will now have to fork over money to the government. Perhaps they'll realize that there's no free lunch. Or free Obamaphone. Maybe when they see that government really does cost them money, some will join the 'less government' bandwagon.

After last week's election, it's obvious that there's no electoral path to reducing the size and scope of government. So, let's drive off the cliff. (posted 11-13-12, permalink)

The Unbearable Lightness Of Being A Distributor: Once upon a time, my plastics company was an authorized factory distributor for Acrylite acrylic sheet. The Unbearable Lightness Of Being A Distributor: Once upon a time, my plastics company was an authorized factory distributor for Acrylite acrylic sheet.

Acrylite was American Cyanamid's version of Plexiglas. As with many famous brands, the Acrylite business is no longer owned by a U.S.-based corporation. Evonik, a German manufacturer of plastics and specialty chemicals, now owns the biz. Plexiglas - once the flagship offering of Philadelphia-based Rohm & Haas - is now made by Arkema, a French company. Lucite acrylic, a former DuPont product, is now produced by a division of Mitsubishi Rayon.

A recent issue of Plastics Distributor & Fabricator magazine carried an ad for Evonik's Acrylite Online Shop, which sells acrylic sheet, rod and tube direct to anyone, bypassing normal distribution channels.

If you're one of the remaining independent distributors of Acrylite, you probably won't feel good about this new development. But you shouldn't be surprised. It has been happening in other industries, too. The seeds were planted a long time ago.

Industrial distribution of nonperishable goods has a long and successful track record in the U.S. Distributors, wholesalers and re-sellers of products traditionally offered benefits that factories could not. Distributors were local sources of product knowledge, advice and customer service. They also understood regional needs of customers better than most factories and could stock their warehouses accordingly. Distributors offered rapid order fulfillment because they maintained their own local/regional warehouses and offered pick-up or delivery.

Things began to change in the 1980s when large distributors started buying up smaller ones. The growth of mega-distributor chains brought in national policies regarding local inventory management, causing a decline in customer service: "We no longer stock that item here. I'll have to order it from our St. Louis branch. It'll be here in a week or so." Sometimes, they seemed uninterested in selling customers: "We're reducing our number of SKUs and have deleted that item from our entire system. Sorry, don't have it. Can't get it." In the quest for efficiency, many of product experts were let go or reassigned: "Gee, I don't know the answer to that. Try calling the factory."

Customers were not happy and, not surprisingly, many of them embraced direct internet sales when the technology became available.

Mega distributors, faced with stagnating/declining sales, sold off their operations to others - often foreign buyers. For example, Cadillac Plastics, once the largest plastics distributor in the world, now belongs to Saudi Basic Industries Corp.

It's not just about the plastics business. Retail electronics and toys have also experienced shake-ups in how they are distributed. As have many other segments of the retail and wholesale trade.

It's a much different world than it was a generation ago. (posted 8-27-12, permalink)

Keynesian Economics: Wiki says that "Keynesian economics are the group of macroeconomic schools of thought based on the ideas of 20th-century economist John Maynard Keynes."

Most Keynes advocates argue that private sector decisions sometimes lead to inefficient macroeconomic outcomes which require active policy responses by the public sector, particularly monetary policy actions by the central bank and fiscal policy actions by the government to stabilize output over the business cycle.

Here's a simpler explanation:

Buh-Bye Bad Bank: Our Alaska Airlines Visa Signature Card, 'serviced' by Bank of America is no more. We cancelled it late last month. I've had more troubles with this card than any other credit card in my lifetime. Buh-Bye Bad Bank: Our Alaska Airlines Visa Signature Card, 'serviced' by Bank of America is no more. We cancelled it late last month. I've had more troubles with this card than any other credit card in my lifetime.

I could never call up and complain because I didn't know how to yell 'asshole' in the various obscure native languages of BofA's unintelligible customer service representatives.

The tipping point came when Alaska Airlines took away a key benefit - being able to use the annual $110 Companion Fare when booking first-class trips. As of August 1st, annual companion ticket was be restricted to coach fares only. We stopped flying coach when the accommodations became more low-rent and grungy than a 1940s Trailways bus. That translates roughly to United Airlines circa 1995.

Even if Alaska changes its mind, we probably won't return - unless BofA gets dumped from the program. That assumes that the bank stays in business. Douglas McIntyre has expressed doubts, noting that BofA "still faces legal and balance sheet problems, which may force it to raise tens of billions of dollars. This will undermine the share price. The final and most difficult challenge is its exposure to the U.S. real estate market, which is unparalleled among its peers. This, in addition to the unhealed scars from poor management and the global financial collapse, have left Bank of America limping along."

Don't expect me to supply crutches. (posted 8-10-12, permalink)

We Live In Interesting Times: An article in the New York Times reported, "Since median inflation-adjusted family income peaked in 2000 at $64,232, it has fallen roughly 6%. You won't find another 12-year period with an income decline since the aftermath of the Depression."

Why? Well, I'd posit that we have been in the Perfect Storm. This is what happens when you run your banking system like a dysfunctional three-card monte game, outsource all your subassemblies to Asia, close plants in Indiana and Michigan and move production to Mexico, close the tech support center in California and open one in Bangladore ... and vote for politicians who enact policies which make the aforementioned business actions the sensible thing to do. As Scooby Doo would say, "Ruh-roh!" Why? Well, I'd posit that we have been in the Perfect Storm. This is what happens when you run your banking system like a dysfunctional three-card monte game, outsource all your subassemblies to Asia, close plants in Indiana and Michigan and move production to Mexico, close the tech support center in California and open one in Bangladore ... and vote for politicians who enact policies which make the aforementioned business actions the sensible thing to do. As Scooby Doo would say, "Ruh-roh!"

The widespread use of computers and the increased use of online sales and service functions means that clerical and support positions are going away. Such jobs used to provide a very decent living for earnest, smart high school grads and college graduates with unmarketable degrees (Humanities, Social Studies, Poetry, Music, et al). This is the dark side of productivity. When you can post your inventory on the web for prospects to browse and select, you no longer need support staff to answer phones and say, "Let me check our inventory list."

Then there's the proliferation of outsourcing/offshoring. Faced with ever increasing labor regulation, upwardly spiraling health care costs (due in large part to the unreformed U.S. tort system) and the like, many companies are reducing their workforce by subcontracting - often overseas.

The annual cost of mandated Federal regulations for firms with less than 20 employees is estimated at almost $8,000. This does not include the cost of training poorly-educated, near illiterate graduates - products of our failing unionized education system, which turns out near-illiterate slackers with little knowledge and even less work ethic.

Many of those who have not experienced offshoring end up as freelancers with no benefits or job security. Popular alternative euphemisms include 'contingent worker' and 'temp independent consultant'. This is the new workplace world and it means that many well-educated, middle-class folks are now finding themselves 'underemployed', with reduced hours and little if any job security. Much like ditch diggers in the 1920s.

In the past, technological changes simply shifted opportunity within the U.S. As farm jobs were eliminated by mechanization, factories hired more. As factories increased productivity and moved work offshore, more Americans turned to lower-pay jobs in health care and other services. But nothing in any economic database indicates that the supply and demand for workers will intersect at a wage that is socially acceptable. Therein lies the problem.

Low-paying jobs in restaurants, nursing homes and health clubs are hard to automate or outsource and will probably always be around. But how do we make America the Land of Opportunity again?

There are no easy answers. (posted 8-2-12, permalink)

They Should Hire Me: The California Public Employees' Retirement System, the largest public pension fund in the U.S., posted an unimpressive 1% return on its investment for the fiscal year ending June 30. The performance was waaaay below the targeted 7.5% average annual return that the $150.6 billion fund needs to meet its obligations. That percentage sounds both unrealistic and imprudent to me.

CalPERS manages retirement benefits for more than 1.6 million California state and local government employees and their families.

During the same period, my conservative investments (appropriate for my age) produced a 3.2% return. I wish it were better but I did beat the S&P 500 index for the period. (posted 7-19-12, permalink)

Office Space: While I enjoyed Mike Judge's 1999 comedy film of the same name, I wouldn't enjoy being an office building owner these days. Office Space: While I enjoyed Mike Judge's 1999 comedy film of the same name, I wouldn't enjoy being an office building owner these days.

The second quarter national occupancy rate remains stubbornly high at 17.2%. The vacancy rate peaked at 17.6% in Q3 and Q4 2010. In Vancouver WA, the office vacancy rate is currently at 20%.

Because of oversupply and lowered demand, there are very few new office buildings being built in the U.S. and new construction will probably stay low for several years.

Why? Well, top-of-the-heap Class A office buildings - typified by the mirror-glazed towers seen in every city - are occupied by insurance firms, wealth management specialists, attorneys, high-end CPA firms and the like.

Many of these firms are abandoning skyscrapers. Their space requirements are less because many assistants and associates can work from home, thanks to the internet. And these companies need less people because technology has increased employee productivity. Also, businesses are finding that clients are no longer impressed with fancy offices at 'name' addresses. Many former Class A dwellers have moved to lower-cost, shorter-commute, hassle-free business parks in the suburbs. Or to a home office, as I did in back in 1999.

Some of these places are revamped industrial parks, converted to "office parks" when demand for industrial space declined as U.S. manufacturing declined. In the past 40 years, manufacturing employment has dropped by over 40%. (posted 7-9-12, permalink)

Shipping News: Twenty-five years ago, United Parcel Service was pretty much the only game in town. Unless you wanted to trust your package to the vagaries of the Post Office.

In those days, my manufacturing business shipped 200-300 packages per day, depending on the season. UPS was pretty arrogant, with a 'who else are you gonna use' attitude. Then Roadway Package System came to town. Prices were lower than UPS, delivery was more reliable. Suddenly UPS became more customer-friendly and competitive. RPS was later acquired by FedEx; the name was changed to FedEx Ground in 2000.

Discovery Plastics - 1985

I haven't paid a lot of attention to shipping companies since I sold my company. But two recent experiences have indicated that UPS may be returning to its old ways. In both cases, UPS missed their estimated delivery date. I could understand this in the midst of winter or other bad weather. But in neither case was weather a factor as far as I could tell.

In the 1980s, it took a week for a package to travel between the Midwest and the Pacific Northwest. Thirty years later, that delivery time using UPS hasn't changed, although FedEx ground can do it in 3-4 days and USPS Priority Mail can go cross-country in 3-5 days.

The most recent package involved an order placed online Friday night 6/15 with a firm in Frankfort, Kentucky. The retailer had UPS pick it up Tuesday afternoon (6/19). Instead of heading to Louisville, UPS went eastbound to Lexington KY. The next day, my 1.3 pound order traveled to Indianapolis and then on to Hodgkins, IL, near Chicago. The following day (6/21), it left the Chicago area enroute to Spokane WA where it landed on 6/25 at 6:34 am. That afternoon, my package left Spokane and headed to Portland OR using Interstate and non-Interstate roads, arriving at 1:08 am. At 4:30 am, a truck departed the UPS Portland distribution center and traveled to Vancouver, WA, arriving at the small distribution center on St. Johns Rd. a mere 24 minutes later. Then it went "out for delivery" and arrived at my door at 5:45 pm on Tuesday 6/26, a day later than forecast.

While I hesitate to tell UPS how to run its business (they wouldn't pay attention anyway - my little package is only one of the 15 million they handle every day), I would note that I-65 provides a straight shot from Louisville to Chicago and Chicago-Portland is an all-Interstate trip. I bet that's what FedEx Ground does. (posted 7-3-12, permalink)

Get The Hell Outta Here: The Commerce Department is considering naming Arab Americans a "socially and economically disadvantaged minority group" that is eligible for special business assistance. Get The Hell Outta Here: The Commerce Department is considering naming Arab Americans a "socially and economically disadvantaged minority group" that is eligible for special business assistance.

The American-Arab Anti-Discrimination Committee (ADC) petitioned Commerce earlier this year to ask that Arab Americans be made eligible for the Minority Business Development Agency (MBDA), which helps minority entrepreneurs gain access to capital, contracts and trade opportunities.

In other words, this is another money-wasting, useless government agency inefficiently addressing problems which are nonexistent. And discriminating against business owners who do not fit its desired ethnic profile.

The ADC petition cited "discrimination and prejudice in American society resulting in conditions under which Arab-American individuals have been unable to compete in a business world." The group claimed discrimination against Arab Americans increased after the terrorist attacks of 9/11. Yeah, like we've really been boycotting your 7-11s and mall kiosks for the last 11 years. Give me a break.

Get over yourselves. Run a good, sound, ethical business. Earn customers' trust. Those things are the keys to success. This is true for every firm, regardless of who owns it. If you're an Arab and can't handle these fundamental business truths, maybe it's time for you to pack up your couscous recipes, hookah pipes, collection of hijabs and your wife's burkas, then tip your fez goodbye and slither back to the Middle East.

I find it both funny and ironic that Middle Easterners were once known as legendary traders and distribution experts. But if you look at wholesaling and trading in America today, you're more likely to find that such businesses are owned by Jews whose ancestry is European. Why? Because they've learned how to operate good, sound, ethical businesses with little or no government help. In spite of anti-Semetic prejudice.

I bet that pisses off a lot of Arabs. Especially the ones who insist on 'help' because they're being 'discriminated against'. Losers.

Minority Business Development Agency services are now offered to African-Americans, Puerto Ricans, Spanish-speaking Americans, American Indians, Eskimos, Aleuts and others. Wow - when was the last time you said to yourself, 'I'm not buying from that #@%& SOB - he's an Aleut'? Or boycotted Eskimo Pies?

In my almost 50 years in the business world, I've observed that, over the long haul, the most successful small business owners tend to be either whites or Asians. And, while I think it's wrong for the government to offer 'special services' to any business based on ethnicity, the fact is that, if the authorities are going to place 'bets' on potentially successful firms, they should be boosting Asian and white establishments.

But then, that wouldn't be politically correct, would it? (posted 6-6-12, permalink)

Old & Broke: People near retirement age claim they can't afford much once they stop working.

A new study from the Employee Benefit Research Institute has stated, "Many workers report they have virtually no savings and investments. In total, 60% of workers report that the total value of their household's savings and investments, excluding the value of their primary home and any defined benefit plans, is less than $25,000."

The report added, "Americans' confidence in their ability to retire comfortably is stagnant at historically low levels. Just 14% are very confident they will have enough money to live comfortably in retirement."

All those projections done in 1998 by 'retirement specialists' are as out-of-date as the hairstyles in 'Purple Rain'.

The problem is likely even worse because many of these people own homes with little or negative equity. The collapse of the housing bubble and resulting decline in home values have dashed expectations and assumptions. Combine this with an equity market which has gone nowhere in 12 years and CD rates of near-zero and you have a recipe for retirement disaster. As Scooby Do's dog - he must be getting near retirement age - would say, "Ruh-roh!"

During many generations in the past, people about to retire could sell their homes to fund their living costs later in life. No more.

That's why you see Henry Winkler, Robert Wagner and Fred Thompson on television peddling those reverse mortgages. They usually come on right after a Hoveround geezer-scooter commercial. (posted 3-26-12, permalink)

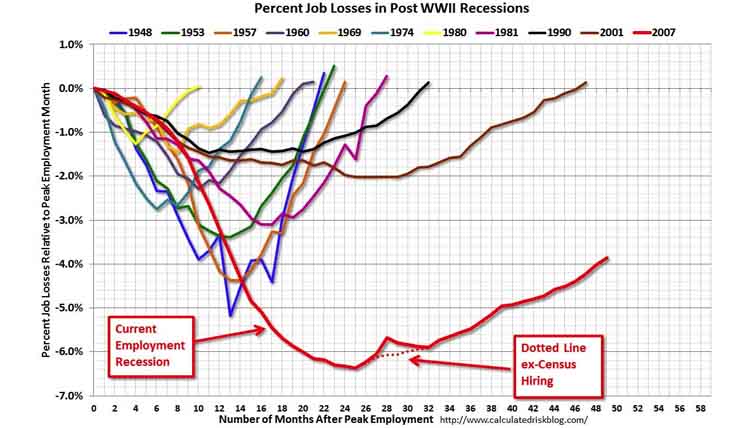

Now This Is A Jobless Recovery: Bill McBride of Calculated Risk has posted a new chart comparing job losses and recovery rates for various post-WWII recessions.

It's an update of this chart, which I had posted in late 2010.

Based on linear projections (assuming that the present recovery continues), it looks like employment will not reach pre-recession levels until August 2014, almost two and a half years from now.

That will make the job loss-recovery cycle a record 89 months - almost seven and one-half years. The previous record time span was for the 2001 recession which clocked in at 46 months and was lambasted by Democrats as a 'jobless recovery'. (posted 3-14-12, permalink)

If You Live In The Real World, You Already Knew This: Forget the alleged 3.1% rise in the Consumer Price Index, the government's widely used measure of inflation. Everyday prices went up 8% over the past year, according to the American Institute for Economic Research. If You Live In The Real World, You Already Knew This: Forget the alleged 3.1% rise in the Consumer Price Index, the government's widely used measure of inflation. Everyday prices went up 8% over the past year, according to the American Institute for Economic Research.

In the 1,000 or so days of the Obama Administration, the price of a gallon of gasoline has jumped 83%, the price of ground beef has gone up 24% and price of bacon has risen 22%.

Scott Grannis has written, "Another thing that doesn't receive as much attention as it should is that Treasury yields have been lower than the rate of PPI inflation for most of the past four years. We haven't seen such low real interest rates since the highly inflationary 1970s, when the Fed was chronically "behind the curve," repeatedly failing to raise interest rates enough to constrain the high inflation that was triggered by the collapse of the dollar early in the decade.

Low real interest rates, a weak dollar, and an accommodative Fed are a combination that augurs for inflation that continues to surprise on the upside for the foreseeable future."

Meanwhile, one-year CDs are yielding 1%, if you're lucky. And the Fed US Federal Reserve says any hike of its key interest rate is unlikely to occur before late 2014. So, don't expect big returns on CDs or money market funds anytime soon.

Several friends of mine have depended on the interest from such fixed income investments to pay their bills in retirement. They've found that their income has dropped by 80% and are now having to dip into the principal for ever-increasing living expenses, causing their nest egg to dwindle at an alarming rate. (posted 3-5-12, permalink)

Dropping Faster Than An Escalade Off A Cliff: Bank of America was the worst performing Dow stock of 2011. Share prices declined by 58.1% in a year. Why so poorly? Well, in my opinion, part of the reason is its spectacularly lousy customer service.

Recently, B of A froze my annual fee credit card because they "detected fraudulent activity." The "activity" consisted of two one-dollar charges by firms I've never heard of. The representative admitted that these firms had attempted to charge tens of thousands of cardholders and that the charges were uniformly refused. Including on my card.

Nevertheless, my airline-affiliated credit card was now no good and a new one "would arrive within 10 days to two weeks." I was told that I could get it faster if I wanted to pay extra. I refused, of course.

My wife and I have already begun using other no-fee credit cards. Our 'new' Bank of America cards have arrived but they won't be experiencing much activity, suspicious or otherwise.

You see, this is not the first time I've had trouble with this B of A credit card. Problems seem to crop up every six months or so. When the annual fee comes due later this year, B of A will be receiving a surprise from us.

If this credit card insanity isn't enough, Bank of America is also "severing lines of credit to some small-business owners who have used them to stay afloat."

The bank is demanding that these customers pay off their credit line balances all at once instead of making monthly payments. "If they can't pay in full, they are being offered new repayment plans for as long as five years, but with far higher interest rates than their original credit lines had."

Finally, it should be noted that - in November, 2011 - Bank of America's board was told by federal bank regulators that the company "could face a public enforcement action if regulators aren't satisfied with recent steps taken to strengthen the bank." (posted 1-5-12, permalink)

Prudent Money Management: Being a senior is no fun these days, especially if you're trying to manage investments. A recent letter to financial columnist Malcolm Berko began, "I'm 76, and my nest egg has dwindled by 55% in the dozen years since I retired. I lost 50% when the tech bubble burst, earned back 80% and lost another 50% in the crash of 2007-2008. Then, I made back about 80% again before losing nearly 35% to the housing bubble."

Wow. First of all, I don't know where this guy's been investing but he must be into some stuff that's either risky or stupid. Or both. In the tech crash of 2000-02, my SEP/IRA dropped by only 17%. By 2007, it was 33% above the 1999 high. The financial meltdown of 2008 caused a scary (to me) 31% drop but I've since recouped my losses and then some.

The letter writer continued, "I've been investing since the early 1960s, and if CDs were paying 5%, I'd cash out and never be in the market again. ... The market is higher than it was in the 1990s, but other folks I talk to tell me that they're also in the minus column."

And there's the rub. CD rates are almost zero as are T-bills. Several friends of mine have depended on the interest from such fixed income investments to pay their bills in retirement. They've found that their income has dropped by 80% and are now having to dip into the principal for living expenses, causing their nest egg to dwindle at an alarming rate.

Meanwhile, television ads from Fidelity Investments - I've seen them on FoxNews and Fox Business - are touting that it's OK to withdraw 4-5% from your retirement account and not worry. Baloney.

An article several years ago in The Motley Fool stated that the "use of a 4% withdrawal rate had a reasonable probability of success only in the 100% S&P 500 and the 75% S&P 500/25% Bond portfolios. None of the portfolios had a good probability of success using a withdrawal rate of 6% or higher save for the shorter payout periods. The 100% bond portfolio failed miserably in comparison with all other portfolios."

Other studies have indicated that the withdrawal rate should be limited to 3% or so if you want complete safety.

My advice: Have an investment stew of mostly stocks (or stock mutual funds) and a sprinkle of bonds (or bond funds). A 3.5% to 4.0% withdrawal rate is the magic number - historically, it's the best assurance that you'll never outlive your money. Even if there's a period of doom ahead:

Prudence pays. (posted 12-14-11, permalink)

Changing Business World; New Middle Class Reality: A post by economist Mark Perry led me to a New York Times article by Thomas Friedman.

I don't always agree with Friedman - his theory of resentment, envy and protest is ill-conceived - but he has made some good observations about the recent drastic sea change in the world of business and how it is profoundly affecting society. Ultimately, it may rearrange the social/political/economic framework more so than the Industrial Revolution of the 19th Century.

"Globalization and the information technology revolution have gone to a whole new level." Friedman noted that "technology and globalization are eliminating more and more 'routine' work - the sort of work that once sustained a lot of middle-class lifestyles."

What's the result of this? Clerical and support positions are going away. Such jobs used to provide a very decent living for earnest, smart high school grads and college graduates with unmarketable degrees (Humanities, Social Studies, Poetry, Music, et al). No more.

"Not only does it take more skill to get a good job, but for those who are unable to raise their games, governments no longer can afford generous welfare support or cheap credit to be used to buy a home for nothing down - which created a lot of manual labor in construction and retail. Alas, for the 50 years after World War II, to be a president, mayor, governor or university president meant, more often than not, giving things away to people. Today, it means taking things away from people."

This is the dark side of productivity. When you can post your inventory on the web for prospects to browse and select, you no longer need support staff to answer phones and say, "Let me check our inventory list." This is the dark side of productivity. When you can post your inventory on the web for prospects to browse and select, you no longer need support staff to answer phones and say, "Let me check our inventory list."

This is another reason why we're experiencing - at best - a jobless recovery.

"The merger of globalization and I.T. is driving huge productivity gains, especially in recessionary times, where employers are finding it easier, cheaper and more necessary than ever to replace labor with machines, computers, robots and talented foreign workers."

The hot word in the corporate world today is Workforce Transformation. Meaning, you'll now be working for us only when we need you. As a freelancer with no benefits or job security. Popular alternative euphemisms include 'contingent worker' and 'temp independent consultant'. This is the new workplace world and it means that many well-educated, middle-class folks are now finding themselves 'underemployed', with reduced hours and little if any job security. Much like ditch diggers in the 1920s.

Mr. Friedman concluded, "We are increasingly taking easy credit, routine work and government jobs and entitlements away from the middle class." We're also taking away their dreams and expectations. (posted 8-19-11, permalink)

Double Dip? In light of the anemic numbers coming out of various government bureaus and the stock market panic, everyone seems to be wondering if we're headed into a double-dip recession. Double Dip? In light of the anemic numbers coming out of various government bureaus and the stock market panic, everyone seems to be wondering if we're headed into a double-dip recession.

The last so-called double dip came in 1980 and '81. I was running my plastics manufacturing and distribution business at the time and never witnessed an uptick and then a fallback. To me, it was one ginormous recession. (Actually, in Linn County Oregon, where my business was once located, it was a full-scale Depression - with unemployment peaking at 27%. During the Great Depression, national unemployment peaked at 27.9% in September 1932.)

My feeling about this time around is that we never came out of the 2008 recession. You can count the many reasons for this but it's a failure of leadership. Alleged gurus like Greenspan, Bernanke, Geithner, Paulson, Summers all played a role in the events leading up to the 2008 collapse or the incompetent fixes offered and tried.

Combine this with one President (Bush) who was asleep at the switch when it came to economic sanity and another (Obama) who is indecisive and clueless when it comes to How The Economy Works and we've now got a major disaster on our hands. Quantitative easing, QE2 and the shovel-ready stimulus programs are abject failures.

The present administration thinks it can 'spend' its way out of the doldrums. That's not the solution; excess spending - and the excess borrowing required to pay for such spending - is the problem. Fiscally, the Tea Party has the right idea: get the government to stop throwing money around. We can no longer afford it. Our government must learn to live within its means.

Next year, we need to elect someone who knows what the Hell he's/she's doing. (posted 8-10-11, permalink)

The Party's Over: The end of the capitalist welfare-state model has arrived. When S&P downgraded the U.S. credit rating, it was the same signal as when the catering manager turns up the house lights, to announce the end of the festivities and spotlight the mess from the wild revelry.

The band has packed up their instruments and left, the overflowing ashtrays are being emptied, the stain-filled tablecloths are on their way to the laundry, the last drunks are staggering outside to vomit copiously in the parking lot and the bill for the party has been presented. We have partied too hard and now find ourselves broke.

The Great Society - aka: the U.S. Welfare State - is pretty much toast. Its failure is living proof that mollycoddling helps no one and greatly harms society. And wrecks our once-vibrant economy.

Winston Churchill once said, "Socialism is a philosophy of failure, the creed of ignorance, and the gospel of envy. Its inherent virtue is the equal sharing of misery."

In this country, it there is now talk of 'Shared Sacrifice', although the liberals who invented this term never specify what exactly society's deadbeats will be 'sacrificing'.

Kurt Schlichter has written, "It's already happening – the liberal dream of a perpetual social welfare state where deadbeat liberal constituencies feed off of the work of productive conservative citizens in perpetuity is dying. There's no doubt about that; the only question left is how long and hard the process will be as the hideous leviathan the utopian liberal establishment has created convulses and dies.

It's going to die hard. And ugly.

The collapse is well-underway in Europe - Greece has gone from the cradle of democracy to a cesspool of union-fueled mobs - but America faces the same trauma."

In this country, we're seeing looters and flash mobs made up mostly of young black bullies. Union thugs physically attack tea party supporters and disrupt town hall meetings.

As to union opposition, Schlichter has noted that "the present crop of union activists aren't the hardscrabble blue collar bruisers of the storied past. Today, most seem to be skinny green tea-sipping public school teachers, naggy Department of Weights & Measures diversity officers, or massive welfare-dispensing office drones clad in form-fitting purple size-XXXXL SEIU t-shirts that were made in China. Not exactly a fearsome crew, unless you're between them and a muffin."

Schlichter has observed, "The DC establishment can ignore math, but math won't ignore it. There is simply not enough wealth that exists or can be imagined into existence through borrowing to support the redistributionist utopia they seek. Greece is a harbinger of the future. The EU will cobble together a bogus bailout that will keep the Hellenic rowboat afloat just a bit longer before it is swamped, but Zorba best learn to swim because it is going under.

Then the other failed states of Europe – Ireland, Spain, Italy, Portugal – will collapse too, taking with them Europe's banks and our banks along with them. The only reason we won't fail first – S&P did not act too early but, rather, far too late in downgrading the U.S. – is that Europe's social democratic elite is even more delusional than ours.

It's over. The system must crash and reboot. The choice is a hard landing or a harder landing."

"The hard part is the entitlements all of us were promised and none of us will ever see. It means repealing Obamacare, but moreover returning the responsibility for health care to where it belongs – the individual. The same with retirement – Social Security is a Ponzi scheme and everyone knows it.

Government student loans, farms subsidies, corporate bailouts, food stamps, Section 8 housing – none of these are federal responsibilities."

Yes, well it's high time for Americans to provide for their own families, businesses and farms. If your business or farm can't make it in the private sector, then you shouldn't be in business for yourself.

If you can't afford a house, go live with relatives, friends or get an apartment. Section 8 housing programs have ruined many communities, bringing blight and crime to formerly peaceful areas.

When we moved into our first home in Willingboro, NJ, the town was a pleasant racially-mixed community with a breadwinner in every home. In the early 1970s, unscrupulous real estate people began pushing Section 8 programs, often submitting fraudulent applications to get approval. Lowlifes arrived from Trenton, Camden, North Philadelphia and other seedy areas bringing with them bad habits, low expectations and a 'gimme' attitude.

Residents saw home values stagnate while houses elsewhere continued to increase in value. Many decided to flee Willingboro. We moved to another town after only five years and felt we got out just in time.

By the early 1980s, the Willingboro Plaza - a once-pleasant shopping center - had become overrun with drug dealers. Muggings, purse snatchings and shoplifting were common. It became so bad that people refused to shop there. Stores closed and the Plaza turned into an abandoned blight. All thanks to The Great Society.

Schlichter concluded, "The key to getting through the coming trauma - and it will be traumatic, as the social contract the liberals unilaterally imposed is rewritten by an implacable reality - is for the productive citizens of the United States to stand firm and stand fast. In other words, just the way Americans have gotten through every other crisis we've faced before.

America's greatest days need not be in the past. Guided by the Founders' vision and the principles of the Constitution, we will find that they lie ahead, over just one more hill."

I hope he's right. (posted 8-9-11, permalink)

Depressing News: Three out of every four Washington residents who have exhausted their full jobless benefits are still unemployed, according to a survey by the Washington State Employment Security Department. Of those who have found jobs, 75% were making less than in their previous jobs - an average of 29% less.

20% of those who found new employment are now working outside the state.

On the national front, Americans cut back on their spending in June for the first time in nearly two years and their incomes grew by the smallest amount in nine months. And, the July ISM Manufacturing Index was at its lowest point in two years.

Here's an example of why our economy is stagnant: Last week, the Boston Globe reported that "Boston Scientific Corp. said yesterday that it plans to eliminate 1,200 to 1,400 jobs worldwide during the next 2 1/2 years to free money for new investments, the Natick medical device maker's second major round of cuts since last year. The company would not say how many jobs will be lost in Massachusetts, where fewer than 2,000 of its 25,000 employees are based."

"Yesterday's move, a day after Boston Scientific disclosed it was investing $150 million and hiring 1,000 people in China, raised fears that the company will gradually shift more work to foreign sites with less government oversight and lower costs than the United States."

The quest for "less government oversight" rings true to anyone who operates a business. The bureaucratic intrusion into everyday commercial activities has become so burdensome that it is killing off business formation and growth.

An article last year in the Wall Street Journal hinted at this when reporting on the impact of Obamacare: "A large swath of the business community opposed the changes, arguing the legislation was too broad and had too many taxes."

"This will make us one of the highest-taxed regions in the world, and that's going to have an impact on the appetite for people to invest in medical innovation," said Bill Hawkins, chief executive of Medtronic Inc., which makes medical devices. He said his company could cut at least 1,000 jobs to absorb a new 2.3% excise tax on medical-device makers.

Thanks again to Barack Obama for helping to kill American business. Well, he did promise change after all. (posted 8-3-11, permalink)

Micro-Economics: Last week we stopped for lunch at a familiar Mexican restaurant we've patronized for 15 years or so. It's in a business park and it used to be that, if you arrived after 11:45 am, you'd have a tough time parking because of all the contractors' trucks. Typically, the place would be full by noon and there would be a line at the counter waiting for phoned-in 'to go' orders.

On this visit, the restaurant was nearly empty. Parking was plentiful. During our lunch, only two other people were being served. There were no pickup orders and the phone didn't ring once while we were there. The business park was nearly empty with lots of 'For Lease' signs on doors. On the way home, we passed several local businesses which have closed their doors.

During the summers from 2000-07, it was tough to get down our street because of all the construction worker trucks. It seemed like everybody was making major home improvements, including us. After 2008, the home improvement merry-go-round stopped dead.

This summer, our street has three contractor jobs going. All are small ones. We're having a few things done - mostly necessary upkeep items. In 2011, we'll probably spend one-tenth of what we spent on home improvements in 2006.

The economy may have bottomed out but the degree of improvement is glacial at best and difficult to notice. (posted 7-19-11, permalink)

What Recovery? Writing in 'Human Events', Jim Hoft has claimed that the Obama 'Recovery' is the worst ever since the Great Depression. "Worst. President. Ever. A new report shows that real GDP has risen 0.8% over the 13 quarters since the recession began, compared to an average increase of 9.9% in past recoveries. Team Obama promised that US GDP growth would be 4.0% in 2011. The Fed announced last week that they see GDP at 2.7% to 2.9% this year."

How bad is it? Take a look at the latest job numbers as well as the updated unemployment graph at Calculated Risk. Things are ugly out there.

"The unemployment rate increased from 9.1% to 9.2%, and the participation rate declined to 64.1%. Note: This is the percentage of the working age population in the labor force." Bill McBride of CR has noted, "The only good news is that June is over."

Keynesians economists worry about the potential instability of the private sector and the undependability of the market driven self-adjustment factor. In his day - during the Great Depression, Keynes said that in times of depression (or deep recessions) the government should focus entirely on spending by injecting the national economy with lots of cash. Well, that got us Hoover Dam and Timberline Lodge but unemployment remained high until we began to gear up for World War II.

We can't use wars - pick any of the three or more we're already in - to save us this time around. (posted 7-11-11, permalink)

Stayin' Alive: A recent article in The Reflector newspaper profiled the Hockinson Market, an establishment that I pass whenever I take my Plymouth on the Hockinson loop drive. The little market is part convenience store and part grocery store. Stayin' Alive: A recent article in The Reflector newspaper profiled the Hockinson Market, an establishment that I pass whenever I take my Plymouth on the Hockinson loop drive. The little market is part convenience store and part grocery store.

The construction business in the Portland/Vancouver metro area remains abysmal; unemployment in the building trades is estimated to exceed 30%. What does this have to do with a little corner market? Read on.

In the article, Jim VanNatta, owner of the Hockinson Market, said that his first dozen years were "nothing but straight up" but, in the last three years, the business has "just tanked." He said that 35% of his business came from construction workers passing by on their way to and from work. VanNatta has struggled to keep the market going in the face of adversity. "Basically, I had to cut back from 11 workers to five."

When one business segment gets in trouble, seemingly unrelated firms get dragged down with it. When a plant closes, retailers that sell work clothes and shoes may go out of business. The Hockinson Market's tale is a lesson in micro-economics.

This country needs to improve its overall business climate - the jobless recovery is killing us all.

The vicious cycle of 'boomlet - big bust' must be broken. The President and Congress must stop dithering and wasting time on 'stimulus programs' that don't work. And they should just shut up about tax increases. And remove some of the burdensome regulatory layers that the government seems to love.

Finally, they should never forget that a healthy economy benefits everyone. (posted 5-23-11, permalink)

Stock Market Gurus: I've been doing some personal financial reviews and came across some old forecasts in my files.

In November 2003, Larry Kudlow wrote: "No one seems to have hit on it yet, but there are many reasons why the current economic recovery could easily develop into an eight or ten-year boom, much like the prosperity cycles of 1982-1990 and 1992-2000." He forecasted a stock rise of "over three-fold, which would translate to a whopping 28,000 Dow Jones Average by 2010!"

Then I found this article from 1998:

The evolution of Mr. Dent's book titles tells quite a story:

• 'The Great Boom Ahead' - published in 1993

• 'The Roaring 2000s' - published in 1998

• 'The Next Great Bubble Boom' - published in 2006

• 'The Great Depression Ahead' - published in 2009

Incidentally, the Dow closed yesterday at 12,548. As I've said before, be skeptical of predictions by 'experts'. (posted 5-17-11, permalink)

Blame Game: Gasoline prices are zooming upward and people are angry. President Obama has ordered an investigation to look for possible culprits. Big, mean oil companies. Evil speculators. Greedy Middle East potentates. Et al.

Well, I've looked at several graphs which show the price of oil in ounces of gold. The graphs are remarkably flat. Over the longer term, oil isn't what's fluctuating. It's the dollar that's fluctuating. And right now, the dollar is in decline because the confidence in America's financial situation is falling.

Since the beginning of 2009, the average dollar retail price of gas has increased 80%. During the same period, the dollar price of gold has increased 71%. The price of gold in U.S. dollars has been increasing steadily since early 2002.

Adam Hamilton has written, "It is fascinating to realize that the Ancient Metal of Kings, gold, has a very strong positive correlation with the King of Commodities, oil, throughout modern history. When oil is strong, gold tends to be strong as well. In fact, the prices of these two commodities are so intertwined over the long term that they seem almost incapable of heading in separate directions over longer strategic timeframes."

Gasoline is not the only retail item on the rise. Over the last year lettuce, bacon, beef, veal, pork, potatoes, tomatoes, milk and coffee have experiences double-digit price increases.

If you're angry about rising gasoline prices, which are going up because the dollar is going down, whom do you blame? Barack Obama? Ben Bernanke? Alan Greenspan? George W. Bush? Barney Frank? Maxine Waters? All of the above?

Don't worry - there's plenty of blame to spread around. Bush's record on increasing the national debt is bad and Obama's is even worse - he of the expensive and totally ineffective stimulus package, "shovel-ready", make-work government jobs, mega-bailouts, etc.

America is rapidly approaching its statutory debt limit - established just last year, when Congress raised it by $1.9 trillion - of $14.3 trillion dollars. Already, we're hearing that action is urgent. If the limit isn't raised again at once, we face possible default on our sovereign obligations, a ruined currency ... blah, blah, blah.

Enough! It is time to freeze the debt. We are broke. Since we can't borrow any more, we must immediately balance the budget. Unaffordable 'entitlements' - Social Security, Medicare, Medicaid, Food Stamps, Extended Unemployment Benefits, Social Programs For Immigrants - must be given a haircut. Right now.

In order to reduce our financial burden (deficit and debt), we must shrink the government. Eliminate federal agencies. The National Endowment of the Arts and the National Education Association would be good places to start. Close 'em down and lay everyone off. Cut the Department of Health and Human Services by half.

We need to cut subsidies, too. Make Amtrak profitable or kill it off. Raise postal rates until the Postal Service is self-sufficient. You get the idea.

Even though the gas price/oil price problem is caused by the fiscal irresponsibility of our elected officials (our Federal budget has more pork than a Reubens nude), I am unable to finish this article without a nod to Frank J. Fleming's ideas about oil drilling. He has asked, "Have we ever tried drilling for oil in Mexico? There should be a decent amount of oil there and some it should be on land so if we spill it, we just get it all over Mexico instead of the ocean.

Now, I know what you're thinking: Won't Mexico be all like, "Hey, that's our oil! You can't drill for it, you pesky gringos!"

Yeah, but then we'll say, "Oh, so now the border means something to you." And we can give Mexico a choice: You can act like a border is meaningful and not encourage people to illegally cross it, or we get to come over and drill all your oil." (posted 5-2-11, permalink)

Bank Shot: In an recent article about Wal-Mart, it was mentioned that the company is still trying to get into the banking business - noting that the retailer "is still in the early stages of banking, hoping to ultimately create a branded bank, much to the vehement opposition of the U.S. banking industry. The company has been twice denied takeovers of banks, but it has expanded its financial services drastically and silently through partnerships with Discover, GE Consumer Finance, MoneyGram International and SunTrust Banks, which entitles its customers to discounted money transfers and check cashing services. Bank Shot: In an recent article about Wal-Mart, it was mentioned that the company is still trying to get into the banking business - noting that the retailer "is still in the early stages of banking, hoping to ultimately create a branded bank, much to the vehement opposition of the U.S. banking industry. The company has been twice denied takeovers of banks, but it has expanded its financial services drastically and silently through partnerships with Discover, GE Consumer Finance, MoneyGram International and SunTrust Banks, which entitles its customers to discounted money transfers and check cashing services.

If the company ever becomes a bank, its footprint would be massive, with an instant 8,500 stores becoming bank branches worldwide. The prospect of Wal-Mart becoming a bank that utilizes the same low margin but high volume approach to financial services horrifies many national banks, which would suffer the same fate as the small general stores Wal-Mart put out of business years ago when they cropped up all over the interstate highways."

This is great news. I have no sympathy for haughty, arrogant banks - the ones who put ATMs outside their doors so that you won't sully their lobby floor in rainy weather. Or spend all their time thinking of ways to convert credit cardholders to debit cards, in yet another attempt to screw-over their customers. This kind of thinking by big banks is nothing new. I've observed such self-serving, anti-depositor behavior for over 50 years.

It will be fun to watch Wal-Mart send a wake up call to lumbering financial behemoths.

Contrary to the lies spread by the anti-Wal-Mart crowd, a study by the Cato Institute has indicated that the presence of a Wal-Mart does not hurt small businesses. In fact, "the slope of the regression line is actually positive and significantly different from zero, which suggests that states with more Wal-Mart stores actually have significantly higher levels of five-to-nine-employee establishments."

So, when someone like Robert Reich claims that Wal-Mart turns "main streets into ghost towns by sucking business away from small retailers," don't believe him.

Most of the people who 'hate' Wal-Mart have never lived in a small town. I have. Such towns are full of merchants offering aging merchandise at remarkably high prices. Store owners are always whining about "people going out of town to buy stuff" and "not supporting the local guy." I used to hear such complaints when I stood in line with these fellow small business owners at Corvallis' miniscule post office in this little Oregon town.

Little did these folks know that I was one of the traitors who traveled elsewhere to buy stuff.

On one occasion, Nickallan's - a local men's store - advertised a 40% off sale on Florsheim shoes. I arrived when the store opened the first day of the sale; there were exactly two pairs of shoes on sale. Some sale. (I guess the reason the extra pair was on sale was so that the store could use the plural form in the ad: "pairs of shoes.") Neither was my size. The owner of this business was active in the local business association and would loudly and frequently rant about the lack of buyer loyalty to "hometown businesses." Nickallan's Men's Traditional Clothing closed in 2006. On one occasion, Nickallan's - a local men's store - advertised a 40% off sale on Florsheim shoes. I arrived when the store opened the first day of the sale; there were exactly two pairs of shoes on sale. Some sale. (I guess the reason the extra pair was on sale was so that the store could use the plural form in the ad: "pairs of shoes.") Neither was my size. The owner of this business was active in the local business association and would loudly and frequently rant about the lack of buyer loyalty to "hometown businesses." Nickallan's Men's Traditional Clothing closed in 2006.

During my 12 years in this little Oregon burg, I never bought a pair of shoes locally. I spent my footwear dollars in Portland, Seattle, New Hampshire and New Jersey - at Terry's Shoe Barn in Rancocas Woods, NJ, a friendly establishment offering great deals on footwear. Terry himself often waited on me. I paid extra to send my purchases home via UPS and still saved money.

Then there was a local Corvallis jewelry store, Coleman Jewelers, who wanted to sell me a widely-discounted name brand watch at full list price. The store didn't even stock any of the line, referring to itself as an "authorized, non-stocking distributor." Huh?

On my next business trip, I bought it for over 25% less - from a chain department store. I'm sure I could have done even better if I had shopped a little harder.

Most of these local merchants paid their help poorly - often minimum wage - and offered few benefits. For many such employees, the opening of a Wal-Mart became a opportunity to move up. Wal-Mart prospered by opening stores in small towns where the 'competition' considered themselves entrenched and were, therefore, indifferent and lazy. Easy pickings.

Wal-Mart helped consumers by raising the retail bar - forcing competitors to improve or go out of business. Soon, it will have the same effect in the banking world. (posted 4-19-11, permalink)

Smokin' Social Security: By the late 1950s, everybody knew smoking caused cancer; people used to jokingly refer to cigarettes as 'coffin nails'.

By the early 1970s, it was common knowledge that Social Security was going broke. People were told "start saving for your own retirement; don't count on Social Security."

Fast forward to today - the cost of Social Security and other entitlement programs is breaking the back of the U.S. Fast forward to today - the cost of Social Security and other entitlement programs is breaking the back of the U.S.

Consider this: According to the Bureau of Economic Analysis, benefits, such as Social Security, food stamps, unemployment insurance and health care, accounted for 16.2% of personal income in the first quarter of 2009 - the highest percentage since the government began compiling records in 1929.

In 1959, total government transfers were only 6.5%. This percentage began to rise as Lyndon Johnson's Great Society kicked in. After peaking in the mid-1970s, it stayed relatively flat percentage-wise until several years ago, when social spending soared to pay for the Medicare drug benefit, expanded health care for children and greater use of food stamps.

The Social Security and Health Insurance segment has grown most rapidly over the last few decades, In 1959, it was 2.5% of personal income. By April 2009, it had grown to 9.5% - almost triple.

I laugh cynically at those chain-smoking morons who sue tobacco companies. Even if you're 70 years old today, you knew smoking was bad for you the day you took your first puff. And now that a lifetime of cigarettes has wrecked your health, you want to blame someone else for your troubles. Sorry for your pain but you've got to take responsibility for your actions.

The same victim mentality can be seen in certain Boomers - now nearing retirement age - who can be seen on television, whining about how they need Social Security to live. They have been enabled by the Social Security Administration, which prints its slogan on the outside of every envelope: 'For the times that count - count on Social Security.'

How come these Boomers, who were still in their twenties when warnings about SS solvency began to emerge, didn't start saving on their own? Well, many did. Good for them. The 72 million Baby Boomers in the U.S. have more discretionary income than any other age group and control 70% of the total net worth - $7 trillion - of American households. Not all yuppies are wastrels.

But those who didn't plan ahead and save are now complaining - to anyone who will listen.

It's hard to work up any sympathy for those who chose the path of the Aesop's squandering grasshopper rather than the thrifty ant. These people blew their money on muscle cars, mood rings, Go-Go boots and Nehru jackets in the 1960s, leisure suits, platform shoes, Bicentennial commemorative crap, designer fragrances and CB radios in the '70s, Swatch watches, Members Only jackets, Walkmans, Cabbage Patch Kids and mesquite-grilled anything in the 1980s, SUVs and dot-com stocks in the '90s. And highly-mortgaged McMansions or vacation homes during the 2000-06 period.

Now, at the end of their working life, these squanderers find themselves nearly broke. And believe that - somehow - it's the government's problem to solve.

Contrary to popular belief, Social Security is not a savings plan where people deposit their money during their working years then withdraw it once they retire. Rather, as Robert Samuelson has described, it is a "pay as you go" scheme. Current workers are taxed to pay current retirees. When these workers retire, they'll then receive money taken forcibly from future workers. Hence, Social Security is "no different than any other Ponzi scheme, except that Americans are compelled to join whether they wish to or not."

For the sake of our children and grandchildren, we must save Social Security. How? Well, one way is for everybody to "take a haircut." By giving people a little less now, Social Security will assuredly be around for future generations. I would suggest the following changes:

• Payouts for current SS recipients are frozen at present levels.

• The cost-of-living allowance should be discontinued for everyone, including those already receiving benefits.

• Anyone born after 1950 won't receive full Social Security benefits until age 67. Currently, such people are eligible at age 66. They can still retire at any time between age 62 and full retirement age, with a reduced payout for early retirement.

• Those born after 1960 will not receive full benefits until age 68. But, they can still retire at any time between age 63 and full retirement age, with a reduced payout for early retirement. At present, such people are eligible for full retirement at age 67.

• Anyone born after 1970 won't receive 100% of their SS benefits until age 70. They can still retire at any time between age 65 and full retirement age, with a reduced payout for early retirement. Under the existing benefit schedule, such people are get full SS benefits at age 67.

Fixing Social Security won't solve all of America's deficit/debt problems. But it will help. (posted 4-15-11, permalink)

A Simple Plan: Yesterday, Wisconsin Republican Rep. Paul Ryan offered his 'Path To Prosperity' debt-reduction program - with a stripped-down budget going forward that includes sweeping changes to federal expenditures, including entitlement spending. Rep. Ryan is trying to have an adult conversation with America about the looming insolvency of the growing welfare state, and he has offered a serious, practical plan to fix it.

Thanks to Paul Ryan, the American people finally have someone offering real Congressional leadership in Washington. President Obama has failed to lead and make tough choices his entire time in the White House. Especially regarding fiscal matters.

No single person or party is responsible for the looming crisis. Yet, the facts are clear: Since President Obama took office, our problems have gotten worse. Major spending increases have failed to deliver promised jobs. The safety net for the poor is coming apart at the seams. Government health and retirement programs are growing at unsustainable rates. The new health-care law is a fiscal train wreck. A complex, inefficient tax code is holding back American families and businesses.

Ryan's is the first serious proposal produced by either party to deal with the overriding money/debt issues of our time.

"This generation's defining moment has arrived," Ryan says in his conclusion. "Government at all levels is mired in debt. Mismanagement and overspending have left a nation on the brink of bankruptcy."

Ryan's plan offers a choice of a sound future. As opposed to no future.

No kidding. In March, the U.S. Government spent eight times what it took in. The federal government grossed $194 billion in tax revenue and paid out $65.898 billion in tax refunds (including $62.011 to individuals and $3.887 to businesses) thus netting $128.179 billion in tax revenue for March.

At the same time, the Treasury paid out a total of $1.1187 trillion. When the $65.898 billion in tax refunds is deducted from that, the Treasury paid a net of $1.0528 trillion in federal expenses for March. This madness cannot continue.

Personally, I think we need more Draconian measures than Ryan has proposed - something even more extreme than the Deficit Reduction Commission scheme. But I can live with Ryan's plan. Every journey begins with a single step. (posted 4-5-11, permalink)

How The Celtic Tiger Died: Michael Lewis has written a lengthy but comprehensive article on the collapse of Ireland's economy. He details how the Emerald Isle went from one of the richest economies in Europe to insolvency in less than a decade.

Morgan Kelly, a professor of economics at University College Dublin, "learned that more than a fifth of the Irish workforce was employed building houses. The Irish construction industry had swollen to become nearly a quarter of the country's GDP - compared with less than 10 percent in a normal economy - and Ireland was building half as many new houses a year as the United Kingdom, which had almost 15 times as many people to house. He learned that since 1994 the average price for a Dublin home had risen more than 500%. In parts of the city, rents had fallen to less than 1% of the purchase price - that is, you could rent a million-dollar home for less than $833 a month."

Lewis continued, "Irish home prices implied an economic growth rate that would leave Ireland, in 25 years, three times as rich as the United States. ("A price/earnings ratio above Google's," as Kelly put it.) Where would this growth come from? Since 2000, Irish exports had stalled, and the economy had been consumed with building houses and offices and hotels."

Fast forward to today: "There are fully finished skyscrapers that sit empty, water pooling on their lobby floors. There's a skeleton of a tower, cranes resting on either side like parentheses, which was meant to house Anglo Irish Bank. There's a city dump for which a developer paid 412 million euros in 2006 - and which is now, when you include the cleanup costs, valued at zero."

I first wrote about Ireland's troubles last year. (posted 2-8-11, permalink)

Mo' Money: Bank Lending to small businesses is finally starting to recover. That's a good thing, especially since the vast majority of new U.S. private-sector jobs are created by small businesses.

Scott Grannis has written, "If, as it appears, bank lending is once again starting to expand, I think that reflects a combination of factors: businesses have finished deleveraging; businesses feel confident enough about the future to expand their borrowings; and banks feel confident enough about the economic climate to expand their lending activity." Scott Grannis has written, "If, as it appears, bank lending is once again starting to expand, I think that reflects a combination of factors: businesses have finished deleveraging; businesses feel confident enough about the future to expand their borrowings; and banks feel confident enough about the economic climate to expand their lending activity."

In May of last year, I wrote, "When I owned a manufacturing business, I needed to borrow funds in order to grow. Most 'ordinary' manufacturing businesses have 30-35% gross profit and net 10% or less before taxes. A 30% growth in sales means that you have to buy 30% more raw material inventory, you'll be carrying 30% more work-in-process and finished goods inventory and your accounts payable will jump by 30% as will your receivables.

Your increase in profit dollars (at 10% NPBT) won't be nearly enough cover these increased expenses. Therefore, if you can't secure working capital, you can't grow and your business will stagnate. Others - your competitors - will step up and meet customer needs."

While my manufacturing business was in the upper quartile of its peers for both net profit before taxes and return on total investment, we borrowed more every year. Our debt as a percentage of net worth was continually decreasing - a healthy condition - but we couldn't grow without access to capital.

When small businesses are denied credit (capital access), the economy stays dead in the water. (posted 1-11-11, permalink)

More 'Finance & the Economy' posts can be found here.

Other Pages Of Interest

copyright 2011-17 - Joseph M. Sherlock - All applicable rights reserved

Disclaimer

The facts presented in this blog are based on my best guesses and my substantially faulty geezer memory. The opinions expressed herein are strictly those of the author and are protected by the U.S. Constitution. Probably.

Spelling, punctuation and syntax errors are cheerfully repaired when I find them; grudgingly fixed when you do.

If I have slandered any brands of automobiles, either expressly or inadvertently, they're most likely crap cars and deserve it. Automobile manufacturers should be aware that they always have the option of trying to change my mind by providing me with vehicles to test drive.

If I have slandered any people or corporations in this blog, either expressly or inadvertently, they should buy me strong drinks (and an expensive meal) and try to prove to me that they're not the jerks I've portrayed them to be. If you're buying, I'm willing to listen.

Don't be shy - try a bribe. It might help.

|

{kind=link}